Building crypto neobanks with Privy

How KAST, UGLYCASH, Avici, and Brookwell are rethinking banking on wallets and stablecoins

Debbie Soon

|Mar 30, 2026

A new generation of financial products is emerging. They look like traditional banks on the surface — accounts, cards, payments — but underneath, they’re built on wallets and stablecoins instead of legacy banking rails.

These are crypto neobanks.

Designed for a global, internet-native world, they give users the ability to store, move, and spend money without relying on traditional financial infrastructure. As the category evolves, they’re going further — introducing programmability, ownership, and new financial primitives that banks were never designed to support.

Across this new wave, one thing is consistent: wallets are becoming the foundation.

What is a crypto neobank?

A crypto neobank combines the usability of modern fintech with crypto infrastructure.

At a high level, they:

Provide familiar interfaces like accounts, cards, and payments

Use wallets as the underlying account layer

Move value using stablecoins instead of traditional rails

Give users more control over their funds, often including key ownership

But not all crypto neobanks are the same. Some focus on accessibility and user experience. Others push further, rebuilding financial systems from first principles — introducing programmability, global-first infrastructure, and increasingly, AI-driven workflows.

Below are four crypto neobanks building on Privy, each taking a different approach to what banking looks like in a wallet-first world.

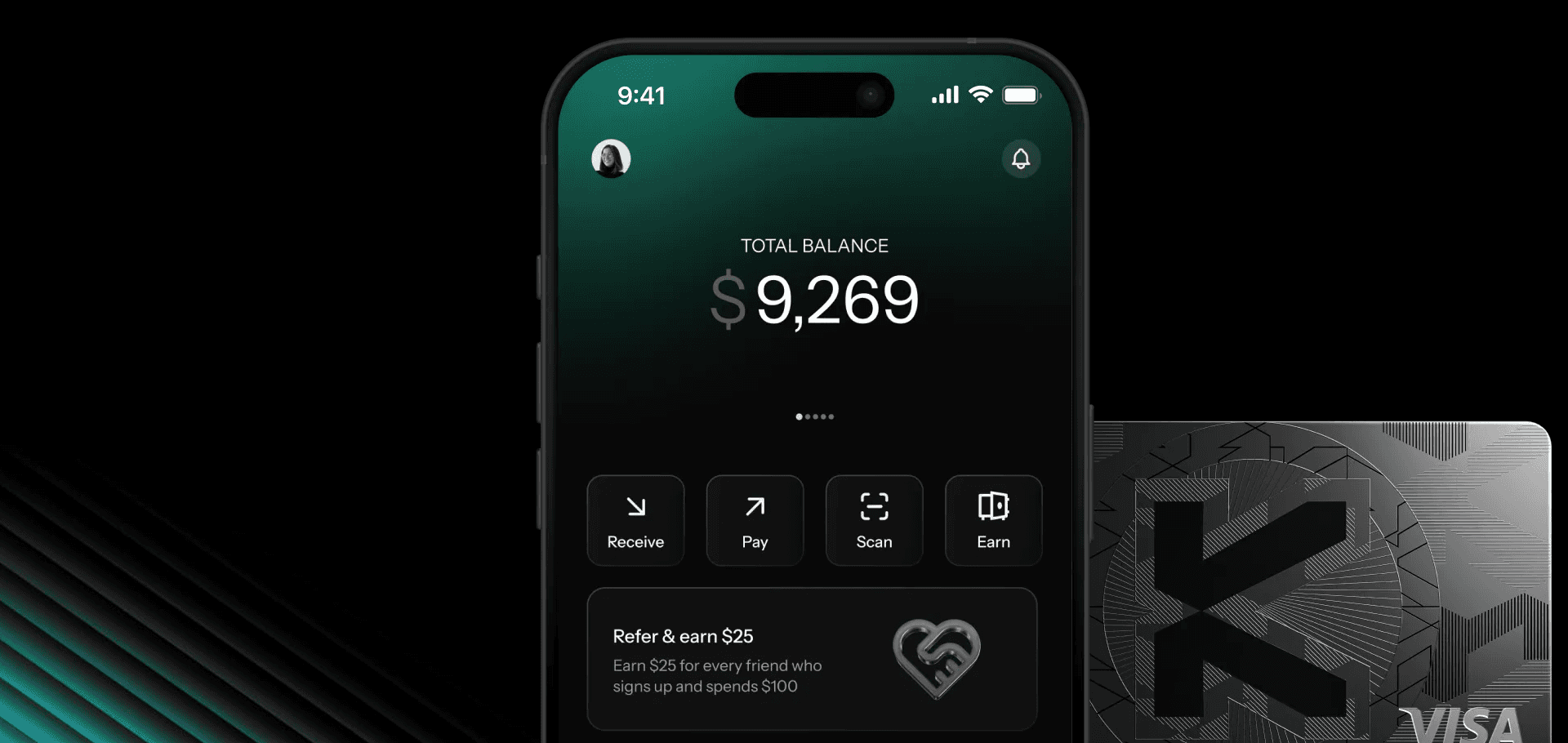

KAST: Bringing crypto into everyday banking

KAST represents one end of the spectrum: making crypto feel like everyday banking.

The product is built around spending. With global accounts and cards, users can hold, send, and spend stablecoins like USDC and USDT anywhere Visa is accepted, turning crypto balances into real-world purchasing power.

What started as a stablecoin-backed card is expanding into a broader financial product, with support for saving and eventually borrowing — all without relying on traditional banking rails.

KAST lowers the barrier to entry by abstracting away complexity. Users don’t need to understand crypto to use it; they just spend as they normally would.

At the same time, KAST leans into partnerships with crypto-native communities and ecosystems, offering rewards, yield opportunities, and perks that connect financial activity with the broader onchain economy.

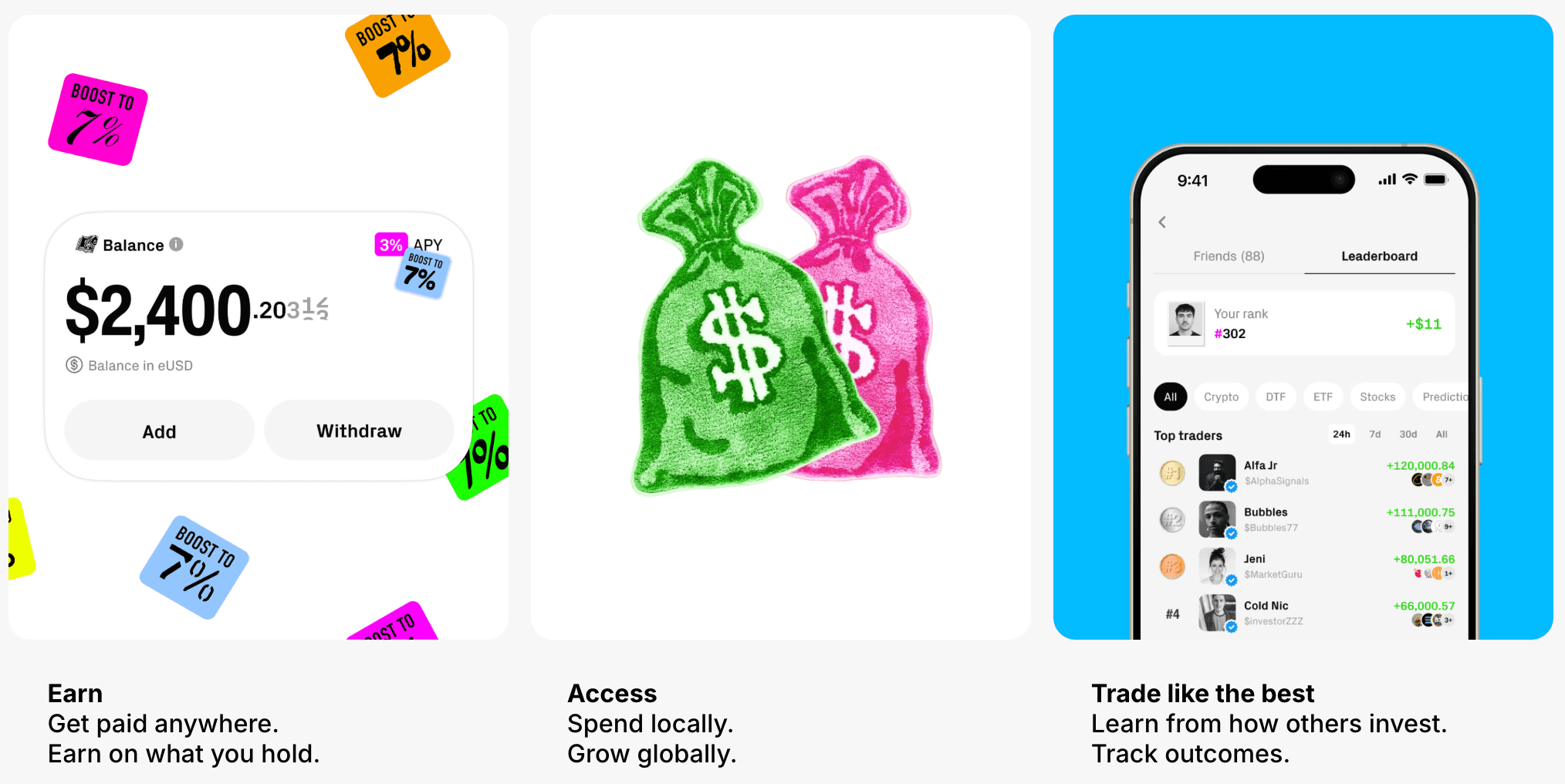

UGLYCASH: Simplifying access to crypto-native money

UGLYCASH takes a different approach: expanding who gets access to financial infrastructure.

Positioned as the opportunity app for a new generation, it’s designed for users who need to earn, move, and grow money across borders without depending on traditional banking systems. The problem isn’t just access to banking. Rather, it’s access to opportunity in a world where income, markets, and communities are already global.

At its core is a unified USD account. Users can open a U.S. virtual account and send or receive payments via ACH, wires, SWIFT, SEPA, SPEI, PIX, and stablecoins — all in one place.

It also introduces new capabilities enabled by crypto rails. With instant payroll, teams can be paid in dollar stablecoins 24/7, with funds settling in seconds and available to spend immediately. Users can move seamlessly between real-world payments, tokenized RWAs, and onchain markets within a single account.

Participation is also built into the UGLYCASH product. Users can access onchain markets, see how others are positioned, and learn from real outcomes — turning financial access into an active, social experience.

Used monthly by over 30,000 people, UGLYCASH reflects a shift from banking as a product to financial opportunity as a platform.

Avici: Rebuilding banking from first principles

Avici pushes beyond interfaces and access, focusing instead on rebuilding the system itself.

It’s building an internet-native neobank designed to connect fiat and crypto while preserving user ownership of funds. Rather than layering crypto onto existing workflows, Avici is rethinking them from the ground up.

Its roadmap includes:

Credit cards and onramp accounts

Lending and borrowing products, from unsecured lending to mortgages

Privacy-focused transactions

Trust score – an onchain FICO alternative credit score

The goal is to create distributed banking infrastructure that fulfills the original promise of crypto by building a financial system that operates without centralized intermediaries.

Avici represents where the category is heading: not just more usable banking, but entirely new financial systems built on different foundations.

"We’re building institutional-grade smart wallets because the future of wallets should look more like modern banking than a single private key. Users need recovery, security abstractions, and programmable permissions. Privy makes this possible at the infrastructure layer, and we’re excited to build together." — Ram K., Founder of Avici

Brookwell: Private, onchain finance for everyday use

Brookwell is building a neobanking app for a new generation of users, focused on making onchain money usable for everyday expenses.

Stablecoins today don’t interface well with systems like rent, phone bills, or mortgages. Brookwell solves this through deep integrations that connect onchain balances to real-world payment flows.

At the same time, users can earn DeFi yield while maintaining the ability to spend, bringing earning and spending into a single financial account.

“We're focused on being the connective tissue between decentralized finance and real-world payments. Our goal is to let users live onchain while seamlessly interfacing with the traditional financial systems they rely on every day." — Ravi Riley, Cofounder & CEO of Brookwell

Brookwell is built on Seismic, a privacy-enabled EVM blockchain designed for fintech. In most onchain systems today, every transaction is publicly visible. Seismic flips that model and allows for every transfer, loan, swap, etc. to be private by default, allowing users to interact with financial services onchain without exposing sensitive data.

Brookwell reflects a new direction for crypto neobanks: financial accounts that are not just global and programmable, but also private by default.

Why wallets, and why Privy

Across KAST, UGLYCASH, Avici, and Brookwell, the products look different. But underneath, they share the same foundation: the wallet is the account.

Instead of accounts held by institutions, crypto neobanks are built on wallets — portable, programmable, and global by default.

That shift unlocks:

Global money movement

Direct ownership of funds

Real-time settlement

Programmable financial logic

Privy provides the wallet infrastructure behind this new generation of financial products.

With Privy, teams can:

Create wallets seamlessly within their apps

Support multiple chains and assets

Define permissions and controls over how funds move

Deliver intuitive onboarding without exposing crypto complexity

Whether you’re building a spending app, a global account, or a new financial system, Privy gives you a single foundation to build on.

The bigger picture

Crypto neobanks are just the beginning. As finance becomes more global and programmable, wallets will replace traditional bank accounts as the default interface for money. Privy powers how those wallets are created, controlled, and embedded into real applications.